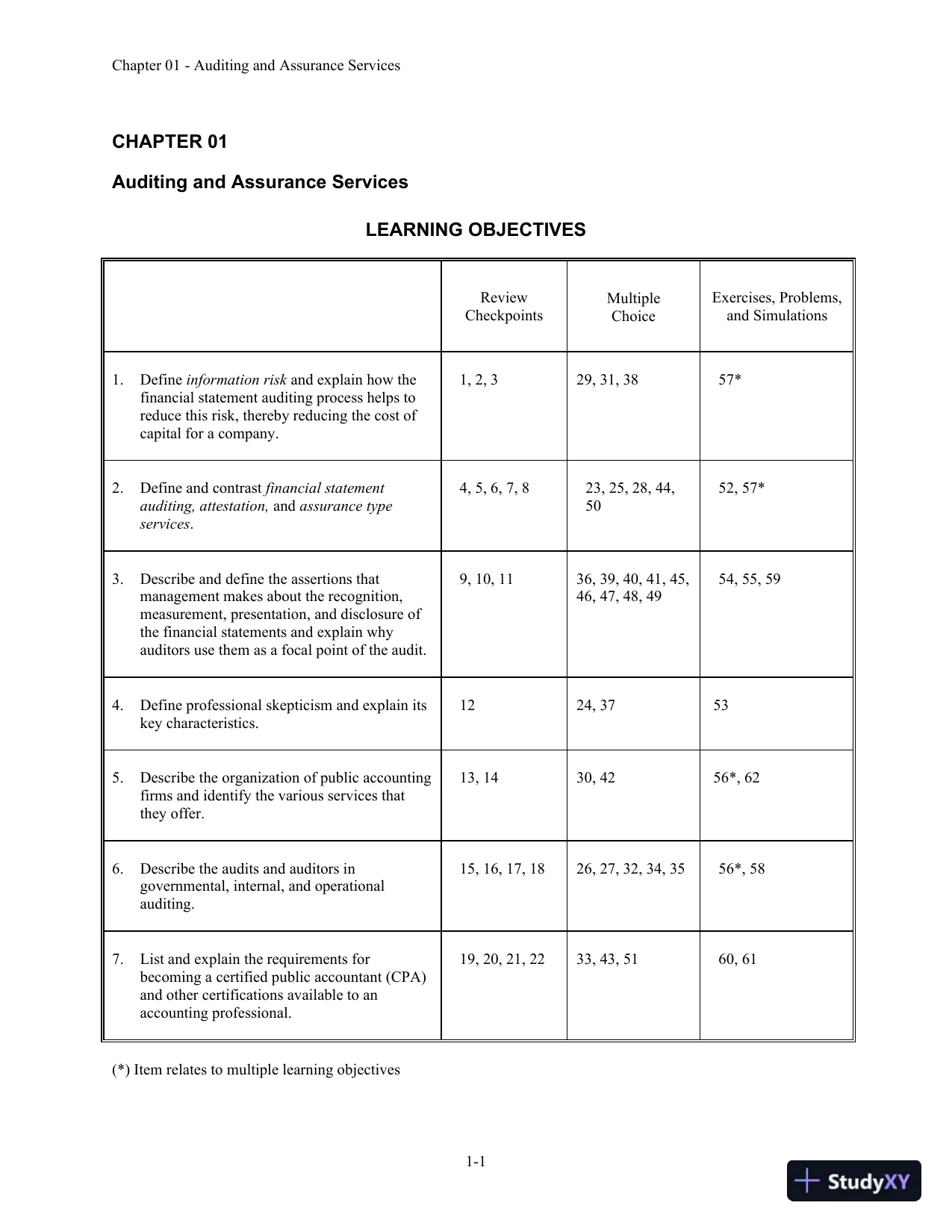

Chapter 01-Auditing and Assurance Services1-1CHAPTER01Auditing and Assurance ServicesLEARNING OBJECTIVESReviewCheckpointsMultipleChoiceExercises, Problems,and Simulations1.Defineinformation riskand explain how thefinancial statement auditing process helps toreduce this risk, thereby reducing the cost ofcapital for a company.1, 2, 329, 31, 3857*2.Define and contrastfinancial statementauditing, attestation,andassurance typeservices.4, 5, 6, 7, 823, 25, 28, 44,5052, 57*3.Describe and define the assertions thatmanagement makes about the recognition,measurement, presentation, and disclosure ofthe financial statements and explain whyauditors use them as a focal point of the audit.9, 10, 1136, 39, 40, 41, 45,46, 47, 48, 4954,55, 594.Define professional skepticism and explain itskey characteristics.1224, 37535.Describe the organization of public accountingfirms and identify the various services thatthey offer.13, 1430, 4256*,626.Describe the audits and auditors ingovernmental, internal, and operationalauditing.15, 16, 17, 1826, 27, 32, 34, 3556*, 587.List and explain the requirements forbecoming acertified public accountant (CPA)and other certifications available to anaccounting professional.19, 20, 21, 2233, 43,5160,61(*) Item relates to multiple learning objectives

Chapter 01-Auditing and Assurance Services1-1CHAPTER01Auditing and Assurance ServicesLEARNING OBJECTIVESReviewCheckpointsMultipleChoiceExercises, Problems,and Simulations1.Defineinformation riskand explain how thefinancial statement auditing process helps toreduce this risk, thereby reducing the cost ofcapital for a company.1, 2, 329, 31, 3857*2.Define and contrastfinancial statementauditing, attestation,andassurance typeservices.4, 5, 6, 7, 823, 25, 28, 44,5052, 57*3.Describe and define the assertions thatmanagement makes about the recognition,measurement, presentation, and disclosure ofthe financial statements and explain whyauditors use them as a focal point of the audit.9, 10, 1136, 39, 40, 41, 45,46, 47, 48, 4954,55, 594.Define professional skepticism and explain itskey characteristics.1224, 37535.Describe the organization of public accountingfirms and identify the various services thatthey offer.13, 1430, 4256*,626.Describe the audits and auditors ingovernmental, internal, and operationalauditing.15, 16, 17, 1826, 27, 32, 34, 3556*, 587.List and explain the requirements forbecoming acertified public accountant (CPA)and other certifications available to anaccounting professional.19, 20, 21, 2233, 43,5160,61(*) Item relates to multiple learning objectivesPreview Mode

This document has 562 pages. Sign in to access the full document!