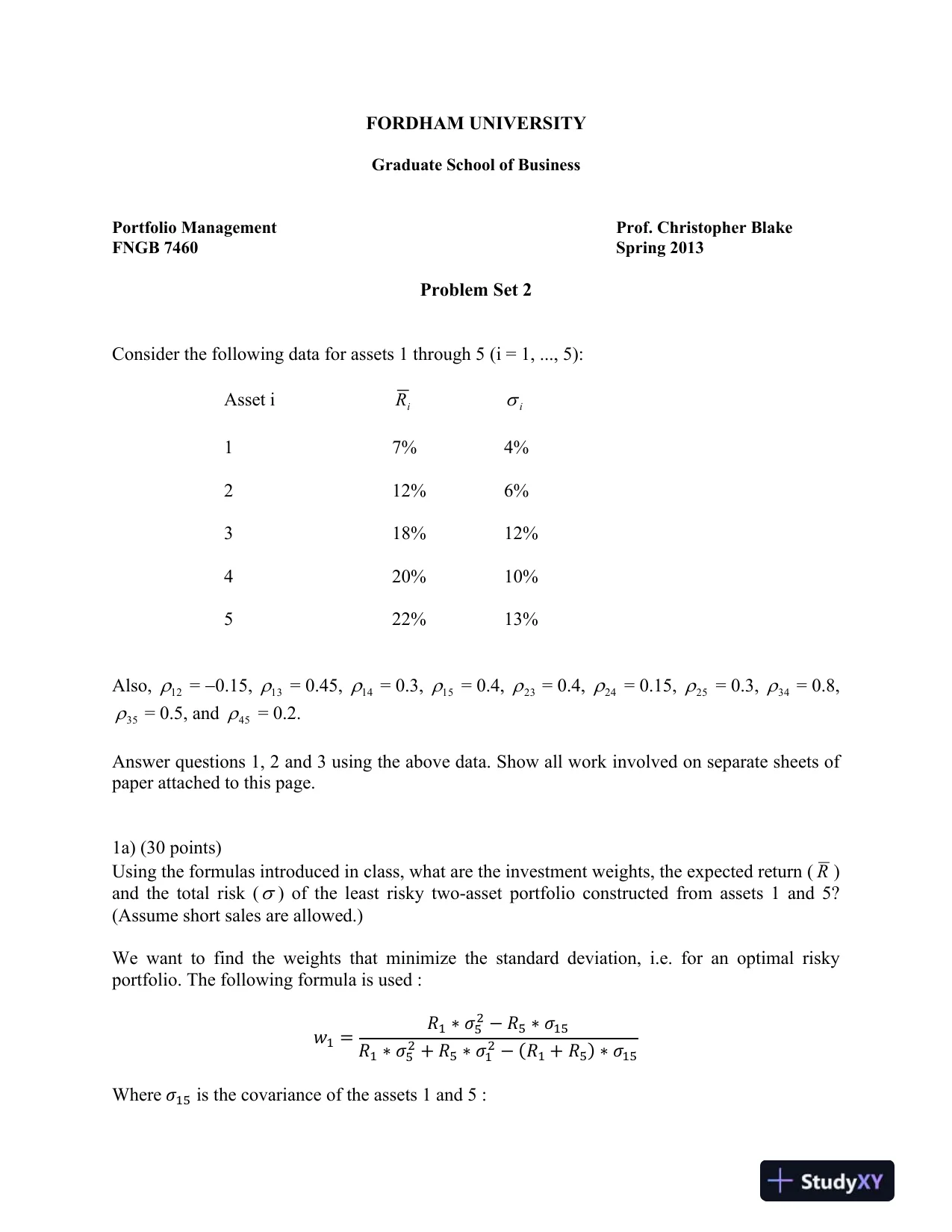

FORDHAM UNIVERSITYGraduateSchool of BusinessPortfolio ManagementProf. Christopher BlakeFNGB 7460Spring2013Problem Set 2Consider the following data for assets 1 through 5 (i = 1, ..., 5):Asset iiRi17%4%212%6%318%12%420%10%522%13%Also,12=−0.15,13= 0.45,14= 0.3,15= 0.4,23= 0.4,24= 0.15,25= 0.3,34= 0.8,35= 0.5, and45= 0.2.Answer questions 1, 2 and 3 using the above data. Show all workinvolved on separate sheets ofpaper attached to this page.1a)(30 points)Using the formulas introduced in class, what are the investment weights, the expected return (R)and the total risk () of the least risky two-asset portfolioconstructed from assets 1 and 5?(Assume short sales are allowed.)We want to find the weights that minimize the standard deviation, i.e. for an optimal riskyportfolio. The following formula is used :𝑤1=𝑅1∗𝜎52−𝑅5∗𝜎15𝑅1∗𝜎52+𝑅5∗𝜎12−(𝑅1+𝑅5)∗𝜎15Where𝜎15is the covariance of the assets 1 and 5 :

FORDHAM UNIVERSITYGraduateSchool of BusinessPortfolio ManagementProf. Christopher BlakeFNGB 7460Spring2013Problem Set 2Consider the following data for assets 1 through 5 (i = 1, ..., 5):Asset iiRi17%4%212%6%318%12%420%10%522%13%Also,12=−0.15,13= 0.45,14= 0.3,15= 0.4,23= 0.4,24= 0.15,25= 0.3,34= 0.8,35= 0.5, and45= 0.2.Answer questions 1, 2 and 3 using the above data. Show all workinvolved on separate sheets ofpaper attached to this page.1a)(30 points)Using the formulas introduced in class, what are the investment weights, the expected return (R)and the total risk () of the least risky two-asset portfolioconstructed from assets 1 and 5?(Assume short sales are allowed.)We want to find the weights that minimize the standard deviation, i.e. for an optimal riskyportfolio. The following formula is used :𝑤1=𝑅1∗𝜎52−𝑅5∗𝜎15𝑅1∗𝜎52+𝑅5∗𝜎12−(𝑅1+𝑅5)∗𝜎15Where𝜎15is the covariance of the assets 1 and 5 :Preview Mode

This document has 5 pages. Sign in to access the full document!