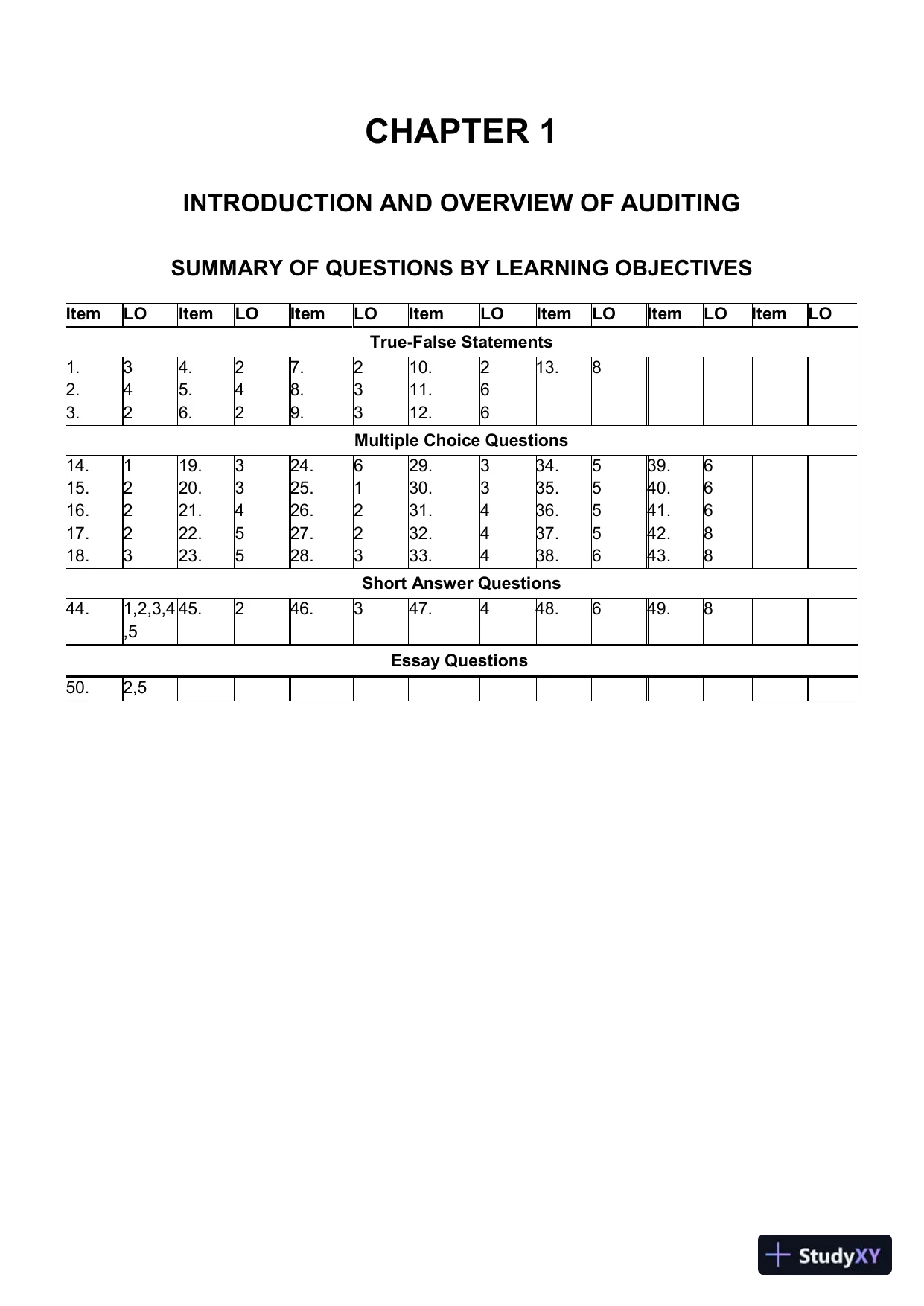

CHAPTER 1INTRODUCTION AND OVERVIEW OF AUDITINGSUMMARY OF QUESTIONS BY LEARNING OBJECTIVESItemLOItemLOItemLOItemLOItemLOItemLOItemLOTrue-False Statements1.34.27.210.213.82.45.48.311.63.26.29.312.6Multiple Choice Questions14.119.324.629.334.539.615.220.325.130.335.540.616.221.426.231.436.541.617.222.527.232.437.542.818.323.528.333.438.643.8Short Answer Questions44.1,2,3,4,545.246.347.448.649.8Essay Questions50.2,5

CHAPTER 1INTRODUCTION AND OVERVIEW OF AUDITINGSUMMARY OF QUESTIONS BY LEARNING OBJECTIVESItemLOItemLOItemLOItemLOItemLOItemLOItemLOTrue-False Statements1.34.27.210.213.82.45.48.311.63.26.29.312.6Multiple Choice Questions14.119.324.629.334.539.615.220.325.130.335.540.616.221.426.231.436.541.617.222.527.232.437.542.818.323.528.333.438.643.8Short Answer Questions44.1,2,3,4,545.246.347.448.649.8Essay Questions50.2,5Preview Mode

This document has 248 pages. Sign in to access the full document!