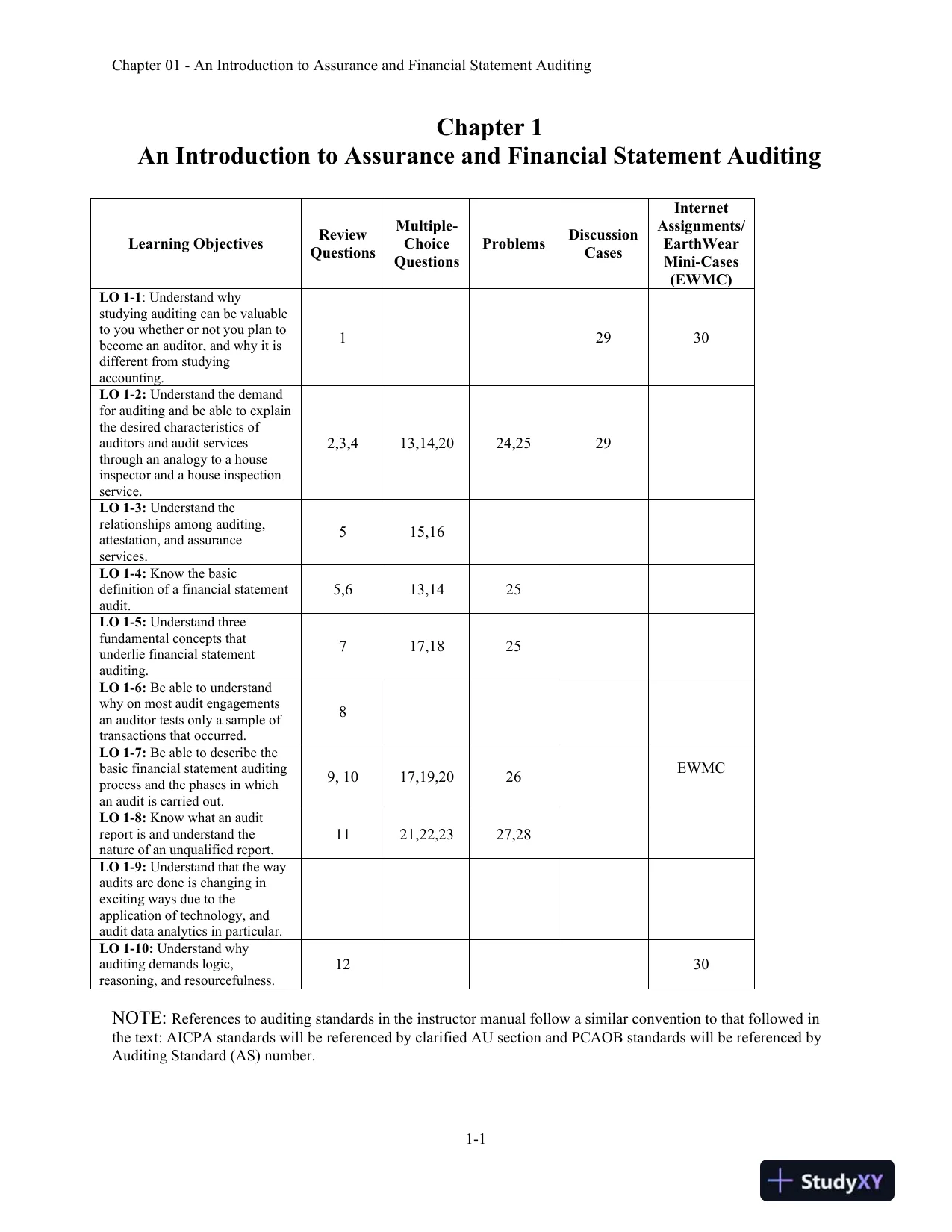

Chapter01-An Introduction to Assurance and Financial Statement Auditing1-1Chapter 1An Introduction to Assurance and Financial Statement AuditingLearning ObjectivesReviewQuestionsMultiple-ChoiceQuestionsProblemsDiscussionCasesInternetAssignments/EarthWearMini-Cases(EWMC)LO1-1: Understand whystudying auditing canbevaluableto youwhether or not you plan tobecome an auditor,and why it isdifferent from studyingaccounting.12930LO1-2:Understand the demandfor auditing andbe able to explainthe desiredcharacteristicsofauditors and audit servicesthrough an analogy to a houseinspector and a house inspectionservice.2,3,413,14,2024,2529LO1-3:Understand therelationships among auditing,attestation,and assuranceservices.515,16LO1-4:Knowthe basicdefinition of a financial statementaudit.5,613,1425LO1-5:Understand threefundamental concepts thatunderlie financial statementauditing.717,1825LO 1-6:Be able to understandwhy on most audit engagementsanauditor tests only a sample oftransactions that occurred.8LO 1-7:Be able to describethebasic financial statement auditingprocess and the phases in whichan audit is carried out.9, 1017,19,2026EWMCLO 1-8:Knowwhat an auditreport is andunderstandthenature of an unqualified report.1121,22,2327,28LO1-9:Understand that the wayaudits are done is changing inexciting ways due to theapplication of technology, andaudit data analytics inparticular.LO 1-10:Understand whyauditing demands logic,reasoning,and resourcefulness.1230NOTE:References to auditing standards in the instructor manual follow a similar convention to that followed inthe text: AICPA standards will bereferenced by clarified AU section and PCAOB standards will be referenced byAuditing Standard (AS) number.

Chapter01-An Introduction to Assurance and Financial Statement Auditing1-1Chapter 1An Introduction to Assurance and Financial Statement AuditingLearning ObjectivesReviewQuestionsMultiple-ChoiceQuestionsProblemsDiscussionCasesInternetAssignments/EarthWearMini-Cases(EWMC)LO1-1: Understand whystudying auditing canbevaluableto youwhether or not you plan tobecome an auditor,and why it isdifferent from studyingaccounting.12930LO1-2:Understand the demandfor auditing andbe able to explainthe desiredcharacteristicsofauditors and audit servicesthrough an analogy to a houseinspector and a house inspectionservice.2,3,413,14,2024,2529LO1-3:Understand therelationships among auditing,attestation,and assuranceservices.515,16LO1-4:Knowthe basicdefinition of a financial statementaudit.5,613,1425LO1-5:Understand threefundamental concepts thatunderlie financial statementauditing.717,1825LO 1-6:Be able to understandwhy on most audit engagementsanauditor tests only a sample oftransactions that occurred.8LO 1-7:Be able to describethebasic financial statement auditingprocess and the phases in whichan audit is carried out.9, 1017,19,2026EWMCLO 1-8:Knowwhat an auditreport is andunderstandthenature of an unqualified report.1121,22,2327,28LO1-9:Understand that the wayaudits are done is changing inexciting ways due to theapplication of technology, andaudit data analytics inparticular.LO 1-10:Understand whyauditing demands logic,reasoning,and resourcefulness.1230NOTE:References to auditing standards in the instructor manual follow a similar convention to that followed inthe text: AICPA standards will bereferenced by clarified AU section and PCAOB standards will be referenced byAuditing Standard (AS) number.Preview Mode

This document has 147 pages. Sign in to access the full document!