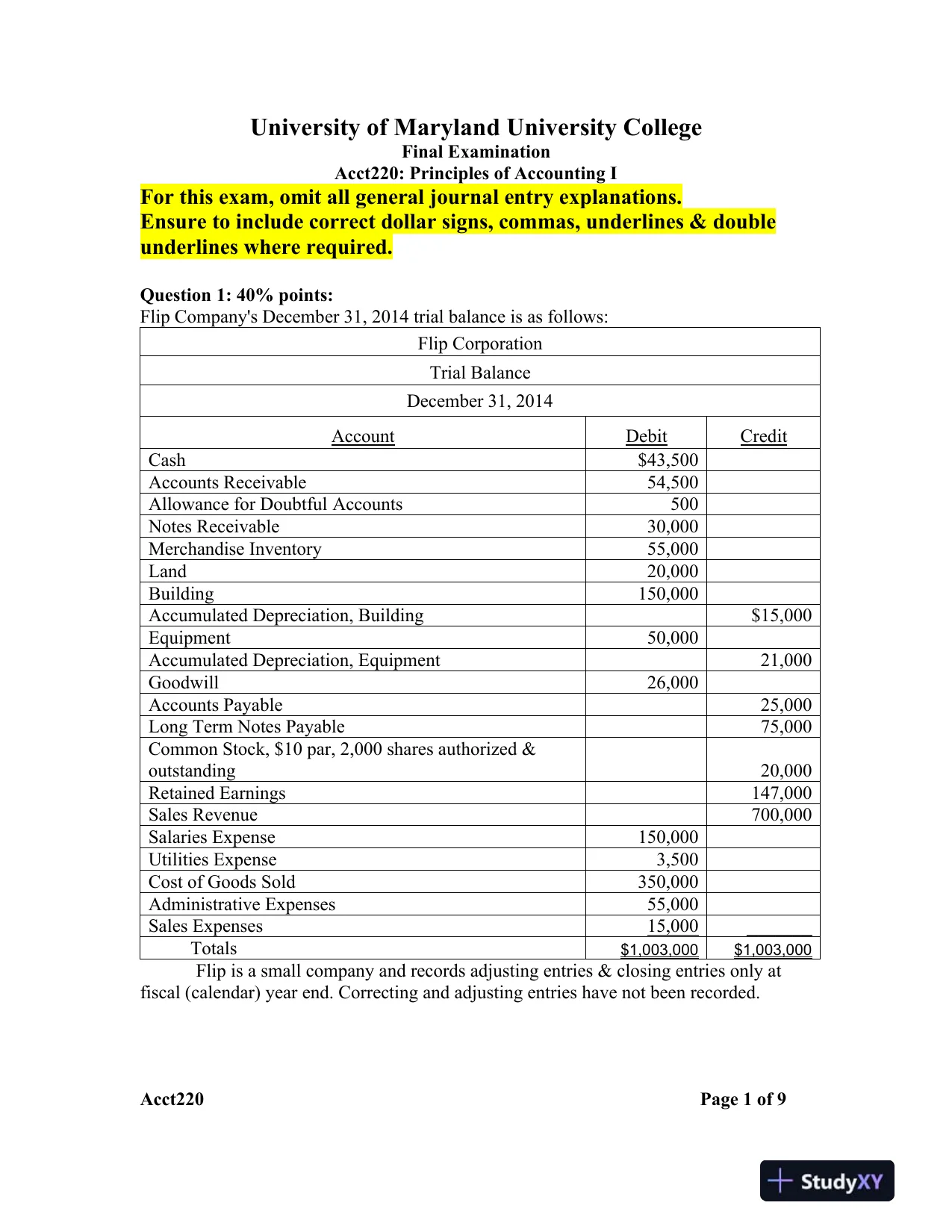

University of Maryland University CollegeFinal ExaminationAcct220:Principles of Accounting IFor this exam, omit all general journal entry explanations.Ensure to include correct dollar signs, commas, underlines & doubleunderlineswhere required.Question1:40%points:Flip Company's December 31, 2014 trial balance is as follows:Flip CorporationTrial BalanceDecember 31, 2014AccountDebitCreditCash$43,500Accounts Receivable54,500Allowance for Doubtful Accounts500Notes Receivable30,000Merchandise Inventory55,000Land20,000Building150,000Accumulated Depreciation, Building$15,000Equipment50,000Accumulated Depreciation, Equipment21,000Goodwill26,000Accounts Payable25,000Long Term Notes Payable75,000Common Stock, $10 par, 2,000 shares authorized &outstanding20,000Retained Earnings147,000Sales Revenue700,000Salaries Expense150,000Utilities Expense3,500Cost of Goods Sold350,000Administrative Expenses55,000Sales Expenses15,000_______Totals$1,003,000$1,003,000Flip is a small company and records adjusting entries & closing entries only atfiscal (calendar) year end.Correctingandadjusting entries havenotbeen recorded.Acct220Page1of 9

University of Maryland University CollegeFinal ExaminationAcct220:Principles of Accounting IFor this exam, omit all general journal entry explanations.Ensure to include correct dollar signs, commas, underlines & doubleunderlineswhere required.Question1:40%points:Flip Company's December 31, 2014 trial balance is as follows:Flip CorporationTrial BalanceDecember 31, 2014AccountDebitCreditCash$43,500Accounts Receivable54,500Allowance for Doubtful Accounts500Notes Receivable30,000Merchandise Inventory55,000Land20,000Building150,000Accumulated Depreciation, Building$15,000Equipment50,000Accumulated Depreciation, Equipment21,000Goodwill26,000Accounts Payable25,000Long Term Notes Payable75,000Common Stock, $10 par, 2,000 shares authorized &outstanding20,000Retained Earnings147,000Sales Revenue700,000Salaries Expense150,000Utilities Expense3,500Cost of Goods Sold350,000Administrative Expenses55,000Sales Expenses15,000_______Totals$1,003,000$1,003,000Flip is a small company and records adjusting entries & closing entries only atfiscal (calendar) year end.Correctingandadjusting entries havenotbeen recorded.Acct220Page1of 9Preview Mode

This document has 10 pages. Sign in to access the full document!