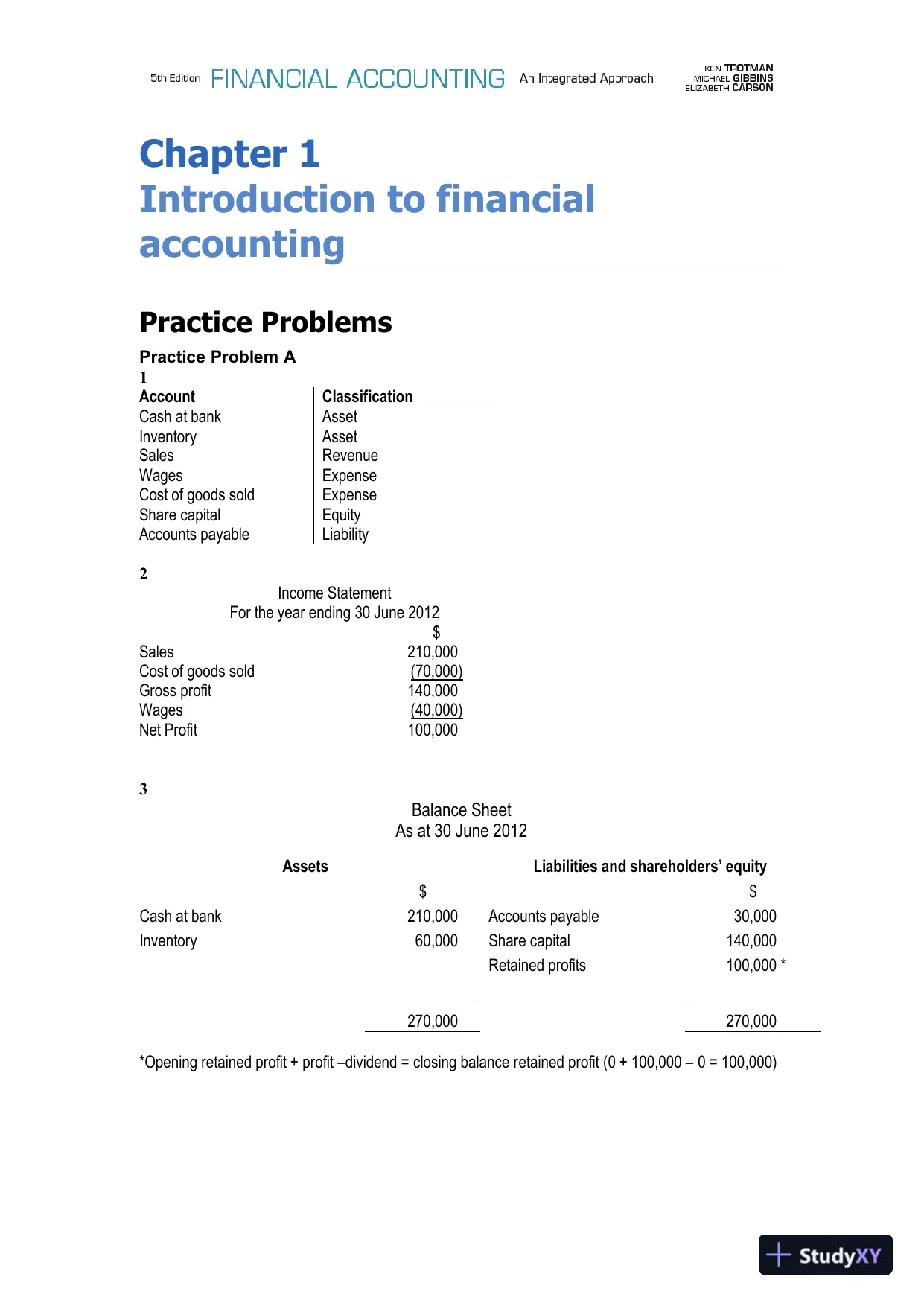

Chapter 1Introduction to financialaccountingPractice ProblemsPractice Problem A1AccountClassificationCash at bankAssetInventoryAssetSalesRevenueWagesExpenseCost of goods soldExpenseShare capitalEquityAccounts payableLiability2Income StatementFor the year ending30 June 2012$Sales210,000Cost of goods sold(70,000)Gross profit140,000Wages(40,000)Net Profit100,0003Balance SheetAs at 30 June 2012AssetsLiabilities and shareholders’ equity$$Cash at bank210,000Accounts payable30,000Inventory60,000Share capital140,000Retained profits100,000 *270,000270,000*Opening retained profit + profit –dividend = closing balance retained profit (0 + 100,000 – 0 = 100,000)

Chapter 1Introduction to financialaccountingPractice ProblemsPractice Problem A1AccountClassificationCash at bankAssetInventoryAssetSalesRevenueWagesExpenseCost of goods soldExpenseShare capitalEquityAccounts payableLiability2Income StatementFor the year ending30 June 2012$Sales210,000Cost of goods sold(70,000)Gross profit140,000Wages(40,000)Net Profit100,0003Balance SheetAs at 30 June 2012AssetsLiabilities and shareholders’ equity$$Cash at bank210,000Accounts payable30,000Inventory60,000Share capital140,000Retained profits100,000 *270,000270,000*Opening retained profit + profit –dividend = closing balance retained profit (0 + 100,000 – 0 = 100,000)Preview Mode

This document has 42 pages. Sign in to access the full document!