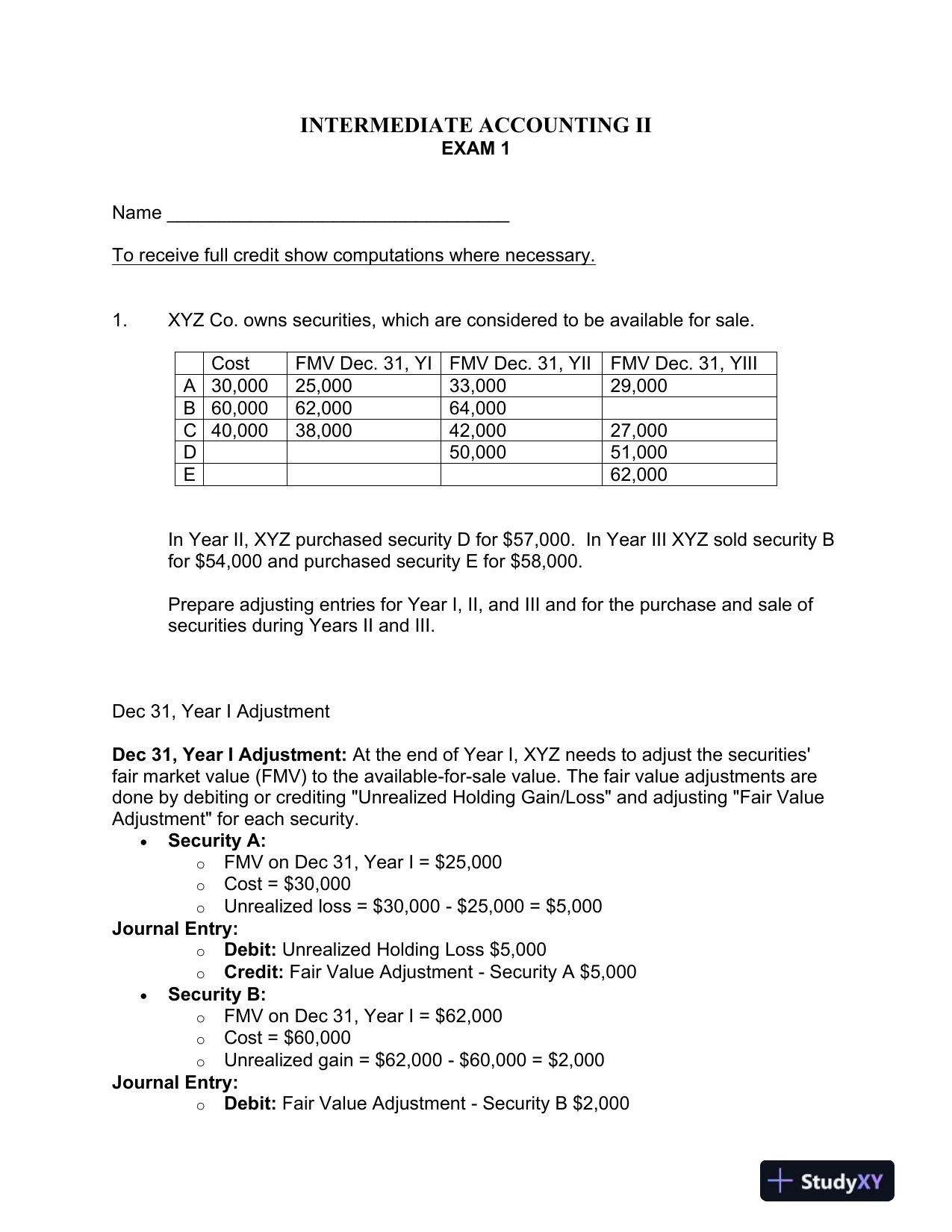

INTERMEDIATEACCOUNTING IIEXAM 1Name_________________________________To receive full credit show computations where necessary.1.XYZ Co. owns securities, which are considered to be available for sale.CostFMV Dec. 31, YIFMV Dec. 31, YIIFMV Dec. 31, YIIIA30,00025,00033,00029,000B60,00062,00064,000C40,00038,00042,00027,000D50,00051,000E62,000In Year II, XYZ purchased security D for $57,000. In Year III XYZ sold security Bfor $54,000 and purchased security E for $58,000.Prepare adjusting entries for Year I, II, and III and for the purchase and sale ofsecurities during Years II and III.Dec 31, YearI AdjustmentDec 31, Year I Adjustment:At the end of Year I, XYZ needs to adjust the securities'fair market value (FMV) to the available-for-sale value. The fair value adjustments aredone by debiting or crediting "Unrealized Holding Gain/Loss" and adjusting "Fair ValueAdjustment" for each security.•Security A:oFMV on Dec 31, Year I = $25,000oCost = $30,000oUnrealized loss = $30,000-$25,000 = $5,000Journal Entry:oDebit:Unrealized Holding Loss $5,000oCredit:Fair Value Adjustment-Security A $5,000•Security B:oFMV on Dec 31, Year I= $62,000oCost = $60,000oUnrealized gain = $62,000-$60,000 = $2,000Journal Entry:oDebit:Fair Value Adjustment-Security B $2,000

INTERMEDIATEACCOUNTING IIEXAM 1Name_________________________________To receive full credit show computations where necessary.1.XYZ Co. owns securities, which are considered to be available for sale.CostFMV Dec. 31, YIFMV Dec. 31, YIIFMV Dec. 31, YIIIA30,00025,00033,00029,000B60,00062,00064,000C40,00038,00042,00027,000D50,00051,000E62,000In Year II, XYZ purchased security D for $57,000. In Year III XYZ sold security Bfor $54,000 and purchased security E for $58,000.Prepare adjusting entries for Year I, II, and III and for the purchase and sale ofsecurities during Years II and III.Dec 31, YearI AdjustmentDec 31, Year I Adjustment:At the end of Year I, XYZ needs to adjust the securities'fair market value (FMV) to the available-for-sale value. The fair value adjustments aredone by debiting or crediting "Unrealized Holding Gain/Loss" and adjusting "Fair ValueAdjustment" for each security.•Security A:oFMV on Dec 31, Year I = $25,000oCost = $30,000oUnrealized loss = $30,000-$25,000 = $5,000Journal Entry:oDebit:Unrealized Holding Loss $5,000oCredit:Fair Value Adjustment-Security A $5,000•Security B:oFMV on Dec 31, Year I= $62,000oCost = $60,000oUnrealized gain = $62,000-$60,000 = $2,000Journal Entry:oDebit:Fair Value Adjustment-Security B $2,000Preview Mode

This document has 18 pages. Sign in to access the full document!