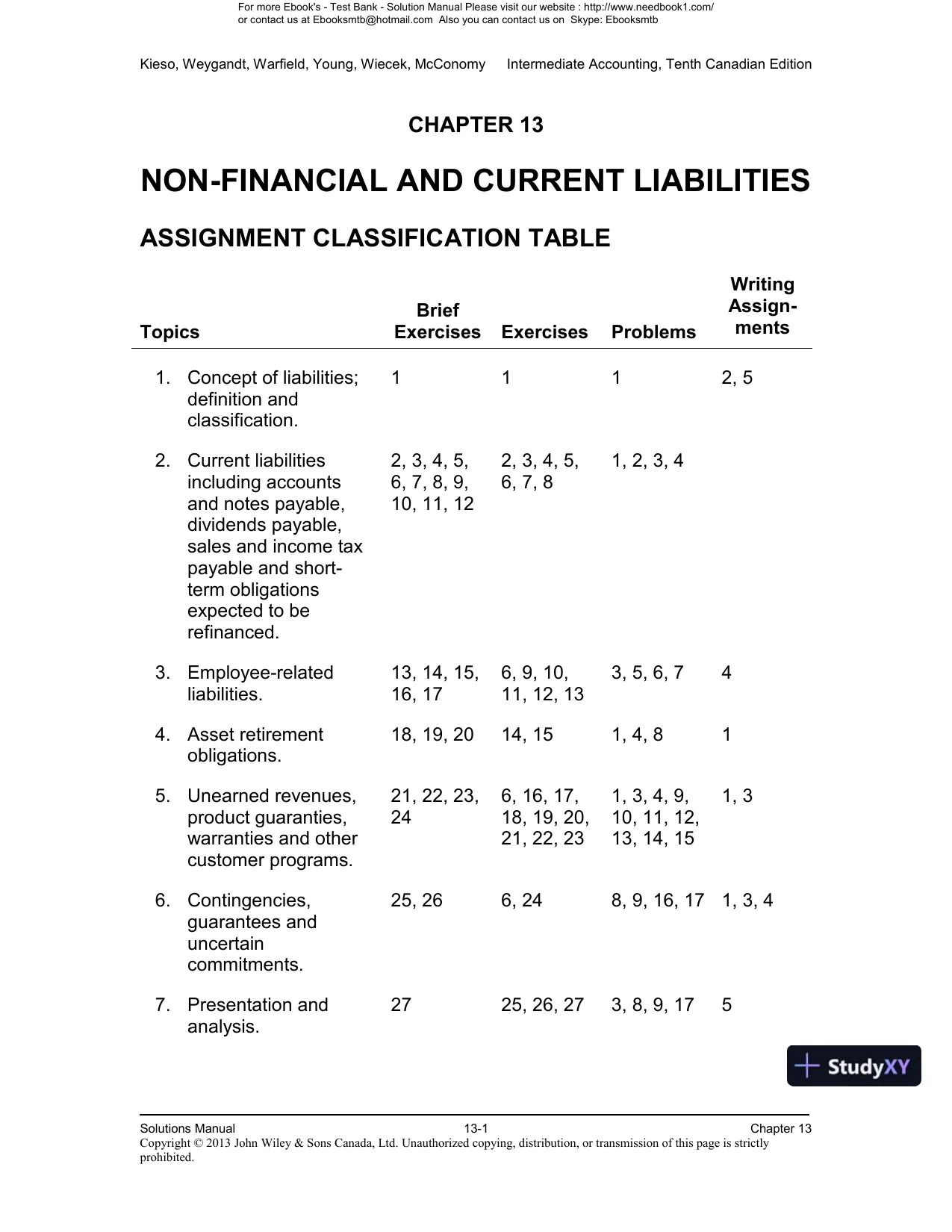

Kieso, Weygandt, Warfield, Young, Wiecek, McConomyIntermediate Accounting, Tenth Canadian EditionCHAPTER 13NON-FINANCIAL AND CURRENT LIABILITIESASSIGNMENT CLASSIFICATION TABLETopicsBriefExercisesExercisesProblemsWritingAssign-ments1.Concept of liabilities;definition andclassification.1112, 52.Current liabilitiesincluding accountsand notes payable,dividends payable,sales and income taxpayable and short-term obligationsexpected to berefinanced.2, 3, 4, 5,6, 7, 8, 9,10, 11, 122, 3, 4, 5,6, 7, 81, 2, 3, 43.Employee-relatedliabilities.13, 14, 15,16, 176, 9, 10,11, 12, 133, 5, 6, 744.Asset retirementobligations.18, 19, 2014, 151, 4, 815.Unearned revenues,product guaranties,warranties and othercustomer programs.21, 22, 23,246, 16, 17,18, 19, 20,21, 22, 231, 3, 4, 9,10, 11, 12,13, 14, 151, 36.Contingencies,guarantees anduncertaincommitments.25, 266, 248, 9, 16, 171, 3, 47.Presentation andanalysis.2725, 26, 273, 8, 9, 175

Kieso, Weygandt, Warfield, Young, Wiecek, McConomyIntermediate Accounting, Tenth Canadian EditionCHAPTER 13NON-FINANCIAL AND CURRENT LIABILITIESASSIGNMENT CLASSIFICATION TABLETopicsBriefExercisesExercisesProblemsWritingAssign-ments1.Concept of liabilities;definition andclassification.1112, 52.Current liabilitiesincluding accountsand notes payable,dividends payable,sales and income taxpayable and short-term obligationsexpected to berefinanced.2, 3, 4, 5,6, 7, 8, 9,10, 11, 122, 3, 4, 5,6, 7, 81, 2, 3, 43.Employee-relatedliabilities.13, 14, 15,16, 176, 9, 10,11, 12, 133, 5, 6, 744.Asset retirementobligations.18, 19, 2014, 151, 4, 815.Unearned revenues,product guaranties,warranties and othercustomer programs.21, 22, 23,246, 16, 17,18, 19, 20,21, 22, 231, 3, 4, 9,10, 11, 12,13, 14, 151, 36.Contingencies,guarantees anduncertaincommitments.25, 266, 248, 9, 16, 171, 3, 47.Presentation andanalysis.2725, 26, 273, 8, 9, 175Preview Mode

This document has 1701 pages. Sign in to access the full document!