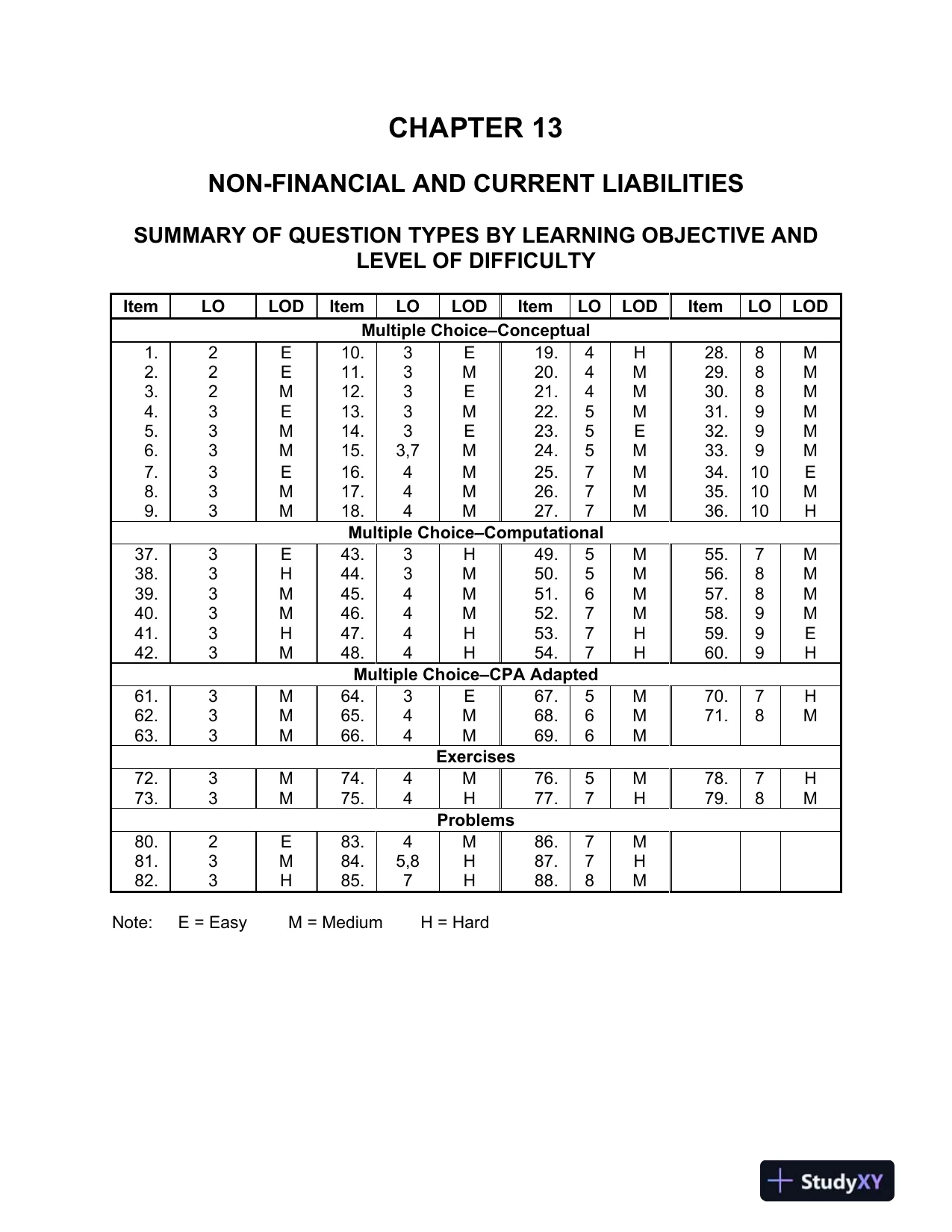

CHAPTER 13NON-FINANCIAL AND CURRENT LIABILITIESSUMMARY OF QUESTION TYPES BY LEARNING OBJECTIVE ANDLEVEL OF DIFFICULTYItemLOLODItemLOLODItemLOLODItemLOLODMultiple Choice–Conceptual1.2E10.3E19.4H28.8M2.2E11.3M20.4M29.8M3.2M12.3E21.4M30.8M4.3E13.3M22.5M31.9M5.3M14.3E23.5E32.9M6.3M15.3,7M24.5M33.9M7.3E16.4M25.7M34.10E8.3M17.4M26.7M35.10M9.3M18.4M27.7M36.10HMultiple Choice–Computational37.3E43.3H49.5M55.7M38.3H44.3M50.5M56.8M39.3M45.4M51.6M57.8M40.3M46.4M52.7M58.9M41.3H47.4H53.7H59.9E42.3M48.4H54.7H60.9HMultiple Choice–CPA Adapted61.3M64.3E67.5M70.7H62.3M65.4M68.6M71.8M63.3M66.4M69.6MExercises72.3M74.4M76.5M78.7H73.3M75.4H77.7H79.8MProblems80.2E83.4M86.7M81.3M84.5,8H87.7H82.3H85.7H88.8MNote:E = EasyM = MediumH = Hard

CHAPTER 13NON-FINANCIAL AND CURRENT LIABILITIESSUMMARY OF QUESTION TYPES BY LEARNING OBJECTIVE ANDLEVEL OF DIFFICULTYItemLOLODItemLOLODItemLOLODItemLOLODMultiple Choice–Conceptual1.2E10.3E19.4H28.8M2.2E11.3M20.4M29.8M3.2M12.3E21.4M30.8M4.3E13.3M22.5M31.9M5.3M14.3E23.5E32.9M6.3M15.3,7M24.5M33.9M7.3E16.4M25.7M34.10E8.3M17.4M26.7M35.10M9.3M18.4M27.7M36.10HMultiple Choice–Computational37.3E43.3H49.5M55.7M38.3H44.3M50.5M56.8M39.3M45.4M51.6M57.8M40.3M46.4M52.7M58.9M41.3H47.4H53.7H59.9E42.3M48.4H54.7H60.9HMultiple Choice–CPA Adapted61.3M64.3E67.5M70.7H62.3M65.4M68.6M71.8M63.3M66.4M69.6MExercises72.3M74.4M76.5M78.7H73.3M75.4H77.7H79.8MProblems80.2E83.4M86.7M81.3M84.5,8H87.7H82.3H85.7H88.8MNote:E = EasyM = MediumH = HardPreview Mode

This document has 434 pages. Sign in to access the full document!