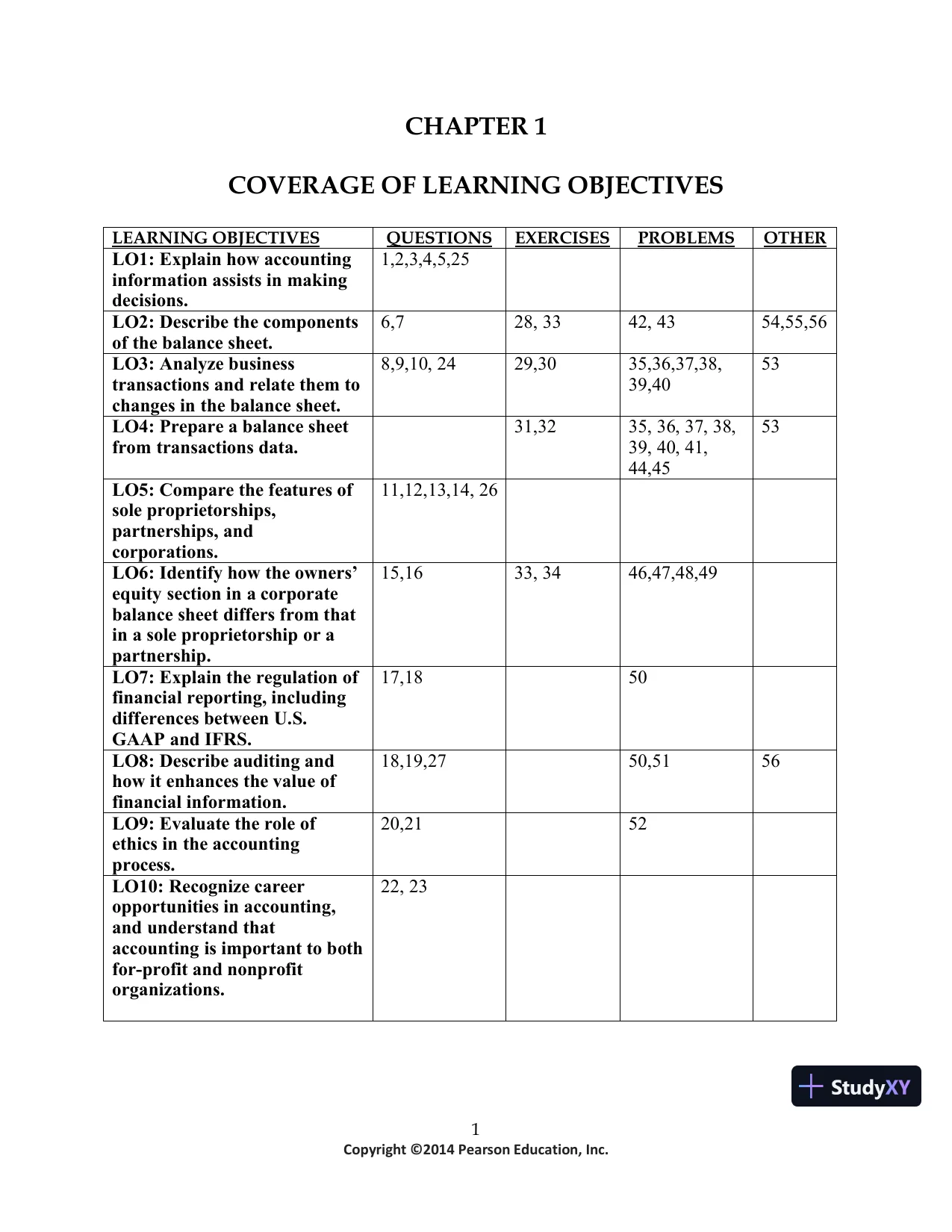

1CHAPTER 1COVERAGE OF LEARNING OBJECTIVESLEARNING OBJECTIVESQUESTIONSEXERCISESPROBLEMSOTHERLO1:Explain how accountinginformation assists in makingdecisions.1,2,3,4,5,25LO2:Describe the componentsof the balance sheet.6,728, 3342, 4354,55,56LO3:Analyze businesstransactions and relate them tochanges in the balance sheet.8,9,10, 2429,3035,36,37,38,39,4053LO4:Prepare a balance sheetfrom transactions data.31,3235, 36, 37, 38,39, 40,41,44,4553LO5:Compare the features ofsole proprietorships,partnerships, andcorporations.11,12,13,14,26LO6:Identify how the owners’equity section in a corporatebalance sheet differs from thatin a sole proprietorship or apartnership.15,1633,3446,47,48,49LO7:Explain the regulation offinancial reporting, includingdifferences between U.S.GAAP and IFRS.17,1850LO8:Describe auditing andhow it enhances the value offinancial information.18,19,2750,5156LO9:Evaluate the role ofethics in the accountingprocess.20,2152LO10:Recognize careeropportunities in accounting,and understand thataccounting is important to bothfor-profit and nonprofitorganizations.22, 23

1CHAPTER 1COVERAGE OF LEARNING OBJECTIVESLEARNING OBJECTIVESQUESTIONSEXERCISESPROBLEMSOTHERLO1:Explain how accountinginformation assists in makingdecisions.1,2,3,4,5,25LO2:Describe the componentsof the balance sheet.6,728, 3342, 4354,55,56LO3:Analyze businesstransactions and relate them tochanges in the balance sheet.8,9,10, 2429,3035,36,37,38,39,4053LO4:Prepare a balance sheetfrom transactions data.31,3235, 36, 37, 38,39, 40,41,44,4553LO5:Compare the features ofsole proprietorships,partnerships, andcorporations.11,12,13,14,26LO6:Identify how the owners’equity section in a corporatebalance sheet differs from thatin a sole proprietorship or apartnership.15,1633,3446,47,48,49LO7:Explain the regulation offinancial reporting, includingdifferences between U.S.GAAP and IFRS.17,1850LO8:Describe auditing andhow it enhances the value offinancial information.18,19,2750,5156LO9:Evaluate the role ofethics in the accountingprocess.20,2152LO10:Recognize careeropportunities in accounting,and understand thataccounting is important to bothfor-profit and nonprofitorganizations.22, 23Preview Mode

This document has 524 pages. Sign in to access the full document!