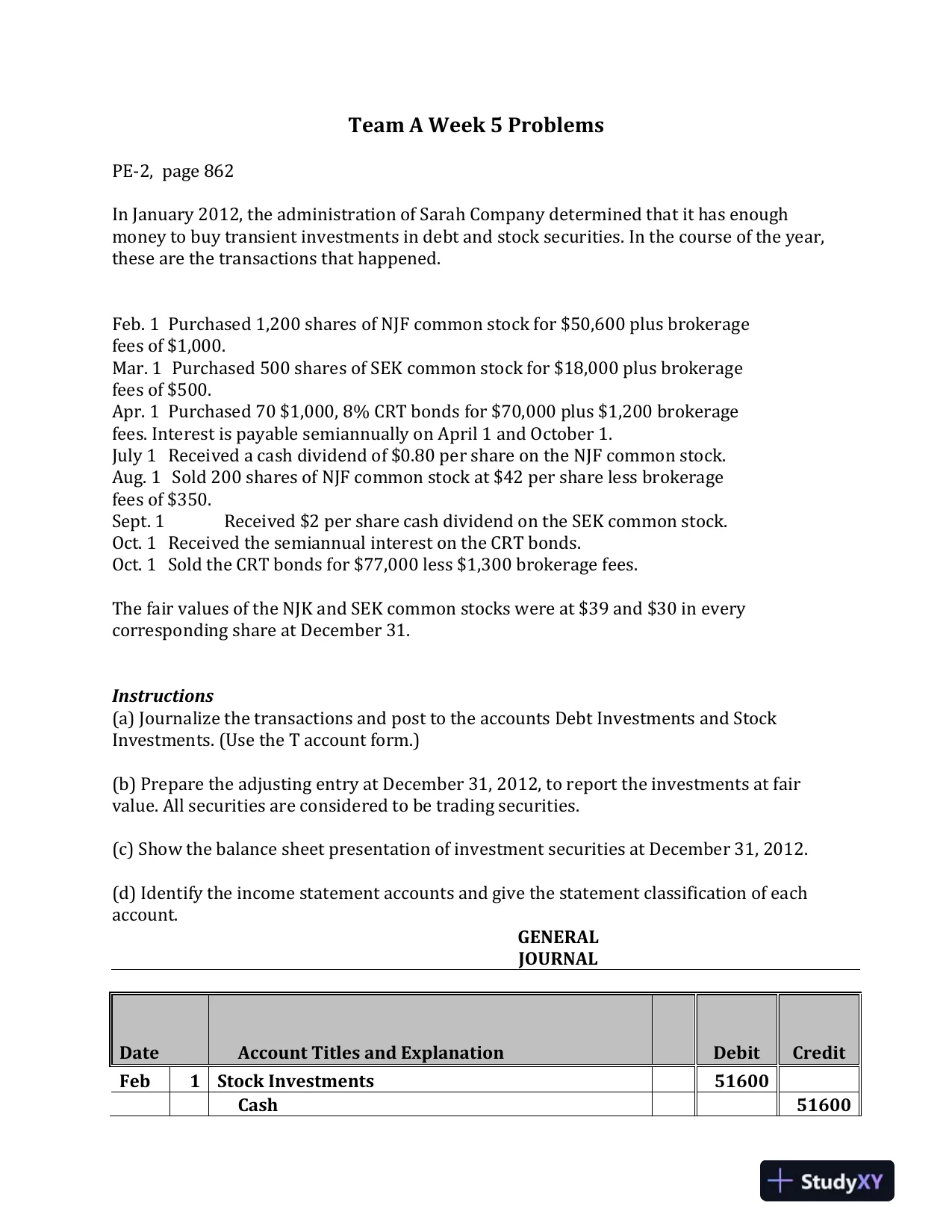

Team A Week 5 ProblemsPE-2, page 862In January 2012, the administration of Sarah Company determined that it has enoughmoney to buy transient investments in debt and stock securities. In the course of the year,these are the transactions that happened.Feb. 1Purchased 1,200 shares of NJF common stock for $50,600 plus brokeragefees of $1,000.Mar. 1Purchased 500 shares of SEK common stock for $18,000 plus brokeragefees of $500.Apr. 1Purchased 70 $1,000, 8% CRT bonds for $70,000 plus $1,200 brokeragefees. Interest is payable semiannually on April 1 and October 1.July 1Received a cash dividend of $0.80 per share on the NJF common stock.Aug. 1Sold 200 shares of NJF common stock at $42 per share less brokeragefees of $350.Sept. 1Received $2 per share cash dividend on the SEK common stock.Oct. 1Received the semiannual interest on the CRT bonds.Oct. 1Sold the CRT bonds for $77,000 less $1,300 brokerage fees.The fair values of the NJK and SEK common stocks were at $39 and $30 in everycorresponding share at December 31.Instructions(a) Journalize the transactions and post to the accounts Debt Investments and StockInvestments. (Use the T account form.)(b) Prepare the adjusting entry at December 31, 2012, to report the investments at fairvalue. All securities are considered to be trading securities.(c) Show the balance sheet presentation of investment securities at December 31, 2012.(d) Identify the income statement accounts and give the statement classification of eachaccount.GENERALJOURNALDateAccount Titles and ExplanationDebitCreditFeb1Stock Investments51600Cash51600

Team A Week 5 ProblemsPE-2, page 862In January 2012, the administration of Sarah Company determined that it has enoughmoney to buy transient investments in debt and stock securities. In the course of the year,these are the transactions that happened.Feb. 1Purchased 1,200 shares of NJF common stock for $50,600 plus brokeragefees of $1,000.Mar. 1Purchased 500 shares of SEK common stock for $18,000 plus brokeragefees of $500.Apr. 1Purchased 70 $1,000, 8% CRT bonds for $70,000 plus $1,200 brokeragefees. Interest is payable semiannually on April 1 and October 1.July 1Received a cash dividend of $0.80 per share on the NJF common stock.Aug. 1Sold 200 shares of NJF common stock at $42 per share less brokeragefees of $350.Sept. 1Received $2 per share cash dividend on the SEK common stock.Oct. 1Received the semiannual interest on the CRT bonds.Oct. 1Sold the CRT bonds for $77,000 less $1,300 brokerage fees.The fair values of the NJK and SEK common stocks were at $39 and $30 in everycorresponding share at December 31.Instructions(a) Journalize the transactions and post to the accounts Debt Investments and StockInvestments. (Use the T account form.)(b) Prepare the adjusting entry at December 31, 2012, to report the investments at fairvalue. All securities are considered to be trading securities.(c) Show the balance sheet presentation of investment securities at December 31, 2012.(d) Identify the income statement accounts and give the statement classification of eachaccount.GENERALJOURNALDateAccount Titles and ExplanationDebitCreditFeb1Stock Investments51600Cash51600Preview Mode

This document has 16 pages. Sign in to access the full document!